OBEROI REALTY: CASH COMPANY IN A HEAVY DEBT WORLD

- Jan 7, 2019

- 3 min read

Current Market Price: 462 Portfolio Weight: 5% Recommendation: BUY

Real Estate sector is at transition phase where the developers who are not well known and have started operation in past four to five years without having expertise in development of projects are now facing issues in construction and are not able to sell units. This will lead to developers who have good brand and knowledge of business to buy land without much competition and benefit from the lower supply as the non-brand developers default.

Out of the scope of listed Real Estate stocks we prefer to OBEROI Realty as it is concentrated to Mumbai Region and has established a well-reputed brand in the region that is able to drive a premium.

As per management this liquidity squeeze is beneficial to them as we explained earlier. The company has made a good portfolio of commercial and residential projects. And has maintained high cash flow levels to manage timely payments of debt and completion of projects.

Rental Income :

The company has received a rental of Rs.150cr in H1FY19 as compared to Rs.113cr in H1FY18, which is 33% growth. EBITDA of the segment is very at 94% and is a direct cash flow to the firm. In Q3FY19 & Q4FY19 , Commerz II will have a higher rental as its occupancy has reached 97% compared to 64% in H1FY19. Company will receive a total Rs350cr annually from 2019-2020.

As per future plans in medium term it is strategising Commerz III which would be at the same land parcel and malls in Borivali & Worli are already on works with deals in pipeline. These together once completed would in total provide the company a total rental income of Rs.1200cr annually.

Residential Projects :

Residential projects are make or break for any real estate company as it requires timely construction specially under RERA and sales are in tranches. Company has been able to maintain good cash flow position even after having majority of portfolio in residential sector. The highest debt to equity ratio has been 0.30x as compared to average industry level of 2-2.5x. The small developers are more indebted by NBFCs as they were purchasing land at record values and their ability to not develop will result in lower supply in medium to long term which would increase prices good brands.

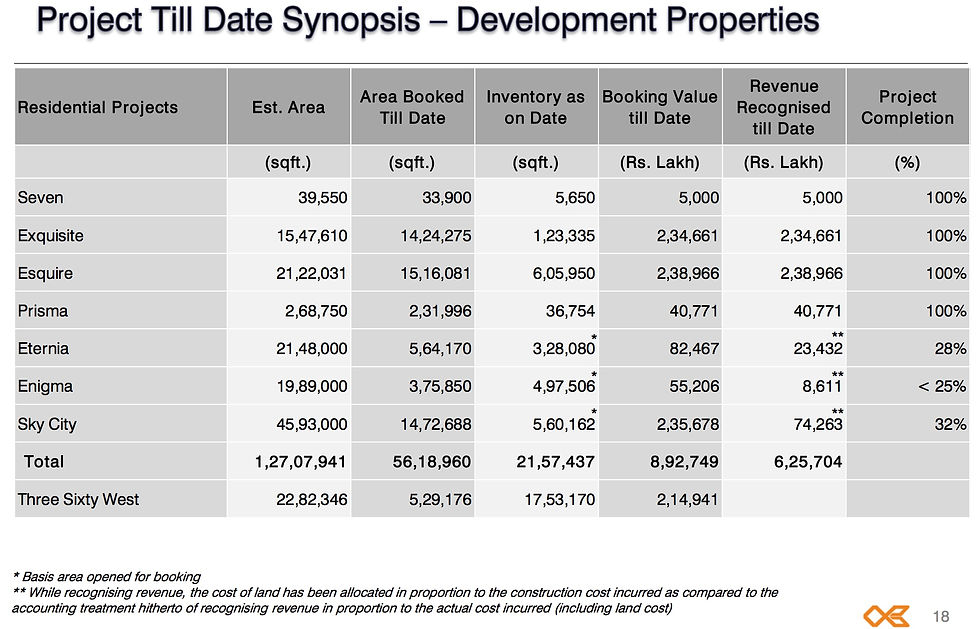

Below is summary of residential projects by the company and its spilt of booking value and revenue recognition.

As per the data above out of 100% project completed only 20% inventory is unsold with majority being in one project that is Esquire. The incomplete projects the unsold inventory is at 57% of the opened for booking. The booking value of incomplete projects is Rs.3734 cr and revenue recognized of the same is Rs1063cr that is 28% of booked value.

These numbers are excluding Three Sixty West projects that have booked value of Rs.2149cr.

Average cost of construction in residential projects currently is Rs4000 per sq.ft. as per management mentioned during concall.

Investment Rationale :

The company has cash and cash equivalents of Rs.1267cr against the total long-term debt of Rs.654cr and short term debt of Rs.309cr making a net cash company after gap of few quarters.

Though due to capex plans for commercial projects the company might raise further debt but keeping a cash flow in check as malls are only started once major tenants are booked with 12 month deposits along with current rental income of Rs.350cr. Plus, the higher completion rate in the Sky City and other projects will lead to higher revenue recognition in coming quarters.

We believe it is well placed to take advantage of the liquidity concerns faced by others and focus cash flow approach helps gain better balance.

Financials :

Comments